The Full Story:

So far, 2023 has surprised investors with its buoyancy. Year to date, the S&P 500 has rallied over 6%, which sounds impressive, but less than the returns of some alternatives. Small-cap US stocks have rallied 8%, developed international stocks nearly 10%, and emerging market stocks almost 12%. Even bonds have begun generating returns again, with the Aggregate Bond index up 3.5% already. These returns have all eclipsed the flat-on-the-year consensus forecasts provided by Wall Street strategists–tune in for our 2023 forecast on February 16th. But for these returns to remain aloft requires inflation to cool, the economy to only slightly recess, and corporate earnings to provide resiliency. This week we received insights into the status of all three.

The Fed’s Favorite Inflation Evaluation

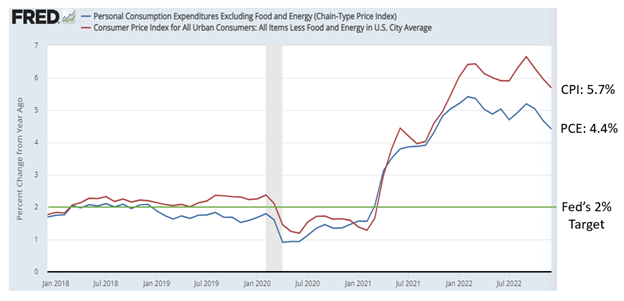

On Friday, the Bureau of Economic Analysis released its most current read on US inflation via the Personal Consumption Expenditures Index (PCE). This index differs from the Consumer Price Index (CPI) calculated by the Bureau of Labor Statistics. While the Consumer Price Index sources its data from consumers via household surveys, the PCE sources its data from suppliers. While the CPI only covers out-of-pocket expenses for consumers, the PCE includes payments on behalf of consumers by businesses and governments. This makes it somewhat less volatile, and a more comprehensive read on inflation, earning it the privilege of being the Fed’s preferred measure. Here are the most current readings on two indicators (food and energy):

Fortunately, the PCE inflation index registers lower current inflation than the CPI inflation index at 4.4% vs. 5.7%, respectively. Unfortunately, the Fed’s 2% target remains some distance away. Nonetheless, Friday’s cooler-than-expected reading added a lift to the markets and offered further evidence that inflation has decidedly tacked downward.

In 2022, the US Economy Grew on Queue

The US economy grew 2.9% in the 4th quarter. The growth registered .3% above expectations despite slowing .3% from its 3rd quarter gain. For the year, the US economy grew 2.1%, spot on with its long-term potential growth rate. However, given the Fed’s mission to cool the economy to douse inflation, these numbers appear perversely problematic. However, within the report, much of the gain in GDP stemmed from government spending, trade gains, and inventory builds. Consumers, which account for nearly 70% of GDP, continued to spend, but their spending pace clearly diminished into quarter’s end. Also, the sizable rise in inventories indicates decreasing demand, reducing the need to stockpile further into Q1. If you strip out gains from trade and inventories, US GDP only grew .8%, a much more innocuous read for the Fed. Overall, this positive report without any Fed moving surprises only adds further rally support.

Earnings Down, Surprises Up, Markets Up

While we have only completed 25% of the 4th quarter earnings season, numbers have largely arrived better than expected. While analysts expected a decline in S&P 500 earnings, the decline should be less than feared. Remember, it’s the spread between reality and expectations that moves markets more than reality itself, and 69% of reporting companies have beaten expectations. With 75% of the earnings season yet to go, it’s too early to declare victory. However, the reality of the market rallying through a season of earnings decline is not unprecedented. In fact, bear markets that accompany earnings declines tend to bottom six to nine months before the earnings themselves bottom. With the S&P October low intact, we think that would place the earnings nadir within the 1st half of 2023 right on queue. As long as something exogenous and unforeseen doesn’t clobber corporate earnings, “better than expected” adds rally support even as earnings decline.

Fed-ruary 1

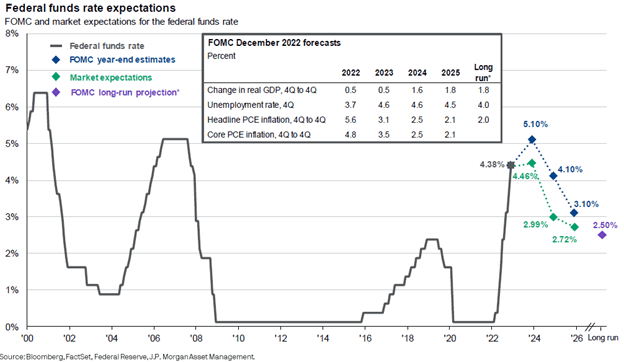

Next week the Fed will raise interest rates .25% to 4.75%. We expect to hear more hawkish refrains about rates being higher for longer, along with some slight acknowledgment that inflation has tempered. Markets will take this in stride as the data released matters more than the Fed’s rhetoric at this point. In fact, the market’s expectation for the Fed’s interest rate policy path now widely diverges from the Fed’s own forecast:

Markets now predict a rate cut by year-end while the Fed foresees adding a couple more increases. This difference of opinion will start pressuring the Fed to relent or lead them to double down on their rhetoric to bring markets to heel. The press conference next week should help with the reconciliation. We will be listening closely… and will report back!

Enjoy your Sunday!

Sources: FRED Database, Bloomberg

">

https://www.wealthstrategists.com/wp-content/uploads/2023/02/WSI_1_29_23.mp3

The Full Story:

So far, 2023 has surprised investors with its buoyancy. Year to date, the S&P 500 has rallied over 6%, which sounds impressive, but less than the returns of some alternatives. Small-cap US stocks have rallied 8%, developed international stocks nearly 10%, and emerging market stocks almost 12%. Even bonds have begun generating returns again, with the Aggregate Bond index up 3.5% already. These returns have all eclipsed the flat-on-the-year consensus forecasts provided by Wall Street strategists–tune in for our 2023 forecast on February 16th. But for these returns to remain aloft requires inflation to cool, the economy to only slightly recess, and corporate earnings to provide resiliency. This week we received insights into the status of all three.

The Fed’s Favorite Inflation Evaluation

On Friday, the Bureau of Economic Analysis released its most current read on US inflation via the Personal Consumption Expenditures Index (PCE). This index differs from the Consumer Price Index (CPI) calculated by the Bureau of Labor Statistics. While the Consumer Price Index sources its data from consumers via household surveys, the PCE sources its data from suppliers. While the CPI only covers out-of-pocket expenses for consumers, the PCE includes payments on behalf of consumers by businesses and governments. This makes it somewhat less volatile, and a more comprehensive read on inflation, earning it the privilege of being the Fed’s preferred measure. Here are the most current readings on two indicators (food and energy):

Fortunately, the PCE inflation index registers lower current inflation than the CPI inflation index at 4.4% vs. 5.7%, respectively. Unfortunately, the Fed’s 2% target remains some distance away. Nonetheless, Friday’s cooler-than-expected reading added a lift to the markets and offered further evidence that inflation has decidedly tacked downward.

In 2022, the US Economy Grew on Queue

The US economy grew 2.9% in the 4th quarter. The growth registered .3% above expectations despite slowing .3% from its 3rd quarter gain. For the year, the US economy grew 2.1%, spot on with its long-term potential growth rate. However, given the Fed’s mission to cool the economy to douse inflation, these numbers appear perversely problematic. However, within the report, much of the gain in GDP stemmed from government spending, trade gains, and inventory builds. Consumers, which account for nearly 70% of GDP, continued to spend, but their spending pace clearly diminished into quarter’s end. Also, the sizable rise in inventories indicates decreasing demand, reducing the need to stockpile further into Q1. If you strip out gains from trade and inventories, US GDP only grew .8%, a much more innocuous read for the Fed. Overall, this positive report without any Fed moving surprises only adds further rally support.

Earnings Down, Surprises Up, Markets Up

While we have only completed 25% of the 4th quarter earnings season, numbers have largely arrived better than expected. While analysts expected a decline in S&P 500 earnings, the decline should be less than feared. Remember, it’s the spread between reality and expectations that moves markets more than reality itself, and 69% of reporting companies have beaten expectations. With 75% of the earnings season yet to go, it’s too early to declare victory. However, the reality of the market rallying through a season of earnings decline is not unprecedented. In fact, bear markets that accompany earnings declines tend to bottom six to nine months before the earnings themselves bottom. With the S&P October low intact, we think that would place the earnings nadir within the 1st half of 2023 right on queue. As long as something exogenous and unforeseen doesn’t clobber corporate earnings, “better than expected” adds rally support even as earnings decline.

Fed-ruary 1

Next week the Fed will raise interest rates .25% to 4.75%. We expect to hear more hawkish refrains about rates being higher for longer, along with some slight acknowledgment that inflation has tempered. Markets will take this in stride as the data released matters more than the Fed’s rhetoric at this point. In fact, the market’s expectation for the Fed’s interest rate policy path now widely diverges from the Fed’s own forecast:

Markets now predict a rate cut by year-end while the Fed foresees adding a couple more increases. This difference of opinion will start pressuring the Fed to relent or lead them to double down on their rhetoric to bring markets to heel. The press conference next week should help with the reconciliation. We will be listening closely… and will report back!

Enjoy your Sunday!

Sources: FRED Database, Bloomberg

">Rally Hat Trick?The Full Story:

So far, 2023 has surprised investors with its buoyancy. Year to date, the S&P 500 has rallied over 6%, which sounds impressive, but less than the returns of some alternatives. Small-cap US stocks have rallied 8%, developed international stocks nearly 10%, and emerging market stocks almost 12%. Even bonds have begun generating returns again, with the Aggregate Bond index up 3.5% already. These returns have all eclipsed the flat-on-the-year consensus forecasts provided by Wall Street strategists–tune in for our 2023 forecast on February 16th. But for these returns to remain aloft requires inflation to cool, the economy to only slightly recess, and corporate earnings to provide resiliency. This week we received insights into the status of all three.

The Fed’s Favorite Inflation Evaluation

On Friday, the Bureau of Economic Analysis released its most current read on US inflation via the Personal Consumption Expenditures Index (PCE). This index differs from the Consumer Price Index (CPI) calculated by the Bureau of Labor Statistics. While the Consumer Price Index sources its data from consumers via household surveys, the PCE sources its data from suppliers. While the CPI only covers out-of-pocket expenses for consumers, the PCE includes payments on behalf of consumers by businesses and governments. This makes it somewhat less volatile, and a more comprehensive read on inflation, earning it the privilege of being the Fed’s preferred measure. Here are the most current readings on two indicators (food and energy):

Fortunately, the PCE inflation index registers lower current inflation than the CPI inflation index at 4.4% vs. 5.7%, respectively. Unfortunately, the Fed’s 2% target remains some distance away. Nonetheless, Friday’s cooler-than-expected reading added a lift to the markets and offered further evidence that inflation has decidedly tacked downward.

In 2022, the US Economy Grew on Queue

The US economy grew 2.9% in the 4th quarter. The growth registered .3% above expectations despite slowing .3% from its 3rd quarter gain. For the year, the US economy grew 2.1%, spot on with its long-term potential growth rate. However, given the Fed’s mission to cool the economy to douse inflation, these numbers appear perversely problematic. However, within the report, much of the gain in GDP stemmed from government spending, trade gains, and inventory builds. Consumers, which account for nearly 70% of GDP, continued to spend, but their spending pace clearly diminished into quarter’s end. Also, the sizable rise in inventories indicates decreasing demand, reducing the need to stockpile further into Q1. If you strip out gains from trade and inventories, US GDP only grew .8%, a much more innocuous read for the Fed. Overall, this positive report without any Fed moving surprises only adds further rally support.

Earnings Down, Surprises Up, Markets Up

While we have only completed 25% of the 4th quarter earnings season, numbers have largely arrived better than expected. While analysts expected a decline in S&P 500 earnings, the decline should be less than feared. Remember, it’s the spread between reality and expectations that moves markets more than reality itself, and 69% of reporting companies have beaten expectations. With 75% of the earnings season yet to go, it’s too early to declare victory. However, the reality of the market rallying through a season of earnings decline is not unprecedented. In fact, bear markets that accompany earnings declines tend to bottom six to nine months before the earnings themselves bottom. With the S&P October low intact, we think that would place the earnings nadir within the 1st half of 2023 right on queue. As long as something exogenous and unforeseen doesn’t clobber corporate earnings, “better than expected” adds rally support even as earnings decline.

Fed-ruary 1

Next week the Fed will raise interest rates .25% to 4.75%. We expect to hear more hawkish refrains about rates being higher for longer, along with some slight acknowledgment that inflation has tempered. Markets will take this in stride as the data released matters more than the Fed’s rhetoric at this point. In fact, the market’s expectation for the Fed’s interest rate policy path now widely diverges from the Fed’s own forecast:

Markets now predict a rate cut by year-end while the Fed foresees adding a couple more increases. This difference of opinion will start pressuring the Fed to relent or lead them to double down on their rhetoric to bring markets to heel. The press conference next week should help with the reconciliation. We will be listening closely… and will report back!

Enjoy your Sunday!

Sources: FRED Database, Bloomberg

" class="link-chevron">The Full Story:

Markets continued to punish the pessimists this week with the S&P 500 now over 4% higher in 2023. Last Friday’s wage disinflation report helped set the trajectory, while this week’s CPI report and better-than-expected earnings from the major banks helped maintain our course. Throughout the year, markets will fixate on the interplay between inflation and earnings. Remember, inflation actually boosts corporate earnings as higher prices drive higher revenues. When inflation falls, revenues fall, leading to corresponding compressions in earnings and, ultimately, stock prices. Analysts calling for disinflation and recession have marked down corporate earnings considerably. We are more optimistic, as corporate executives have had months to prepare for recessionary threats. Proposing that even in light of inflation and a potential recession, earnings resilience could surprise to the upside. This week provided two main data points to help resolve our dispute.

The Consumer Price Index Plunge

The U.S. Bureau of Labor Statistics released its December CPI report on Thursday morning. For the month of December, Consumer Price Inflation fell .1% versus November while gaining 6.5% over the past year. This stands well below the 9% reached in June but still well above the Fed’s 2% target. However, a deeper dig into the report reveals more weakness than the headlines might suggest. Consider the following 3-month average across the goods, services, and shelter components:

Core goods prices have slipped into deflation as new and used auto prices have collapsed, with auto semiconductors more prevalent and logistics bottlenecks cleared. Services excluding shelter inflation have legged lower as COVID revenge travel and dine-outs moderate. Only rent inflation remains truly problematic, but of all the indicators, this lags the most. In fact, if we look at more concurrent indicators like the New Tenant Rent Index and the All Tenant Repeat Rent Index, we find rapid disinflation in rents that will ultimately register in CPI:

In sum, with goods inflation deflating, services ex-rents inflation dis-inflating, and rent poised to fall based upon more current indicators, inflation has clearly committed to a downward trend. Inflation gains over the last three months, annualized at closer to 3%, get us pretty close.

4th Quarter Earnings Yearnings

Earnings season began in earnest on Friday as the major money center banks released their fourth-quarter results. Analysts project S&P 500 earnings to fall 4%, the first quarterly decline since 2020. Only a small portion of the S&P 500 has reported results to date, but so far, the results have proven promising. Of the 29 companies that have reported, 79% have beaten estimates by 7.7%, on average. Should S&P 500 companies grow earnings in the fourth quarter rather than shrink them despite inflation declines, investors may see this as positive foreshadowing for 2023. If so, earnings resiliency spells investment opportunity, which will recalibrate expectations and rerating indices higher.

Have a great Sunday!

Sources: BLS, FRED Database, Bloomberg

">

https://www.wealthstrategists.com/wp-content/uploads/2023/01/WSI_1_15_23-Premiere-Edit.mp3

The Full Story:

Markets continued to punish the pessimists this week with the S&P 500 now over 4% higher in 2023. Last Friday’s wage disinflation report helped set the trajectory, while this week’s CPI report and better-than-expected earnings from the major banks helped maintain our course. Throughout the year, markets will fixate on the interplay between inflation and earnings. Remember, inflation actually boosts corporate earnings as higher prices drive higher revenues. When inflation falls, revenues fall, leading to corresponding compressions in earnings and, ultimately, stock prices. Analysts calling for disinflation and recession have marked down corporate earnings considerably. We are more optimistic, as corporate executives have had months to prepare for recessionary threats. Proposing that even in light of inflation and a potential recession, earnings resilience could surprise to the upside. This week provided two main data points to help resolve our dispute.

The Consumer Price Index Plunge

The U.S. Bureau of Labor Statistics released its December CPI report on Thursday morning. For the month of December, Consumer Price Inflation fell .1% versus November while gaining 6.5% over the past year. This stands well below the 9% reached in June but still well above the Fed’s 2% target. However, a deeper dig into the report reveals more weakness than the headlines might suggest. Consider the following 3-month average across the goods, services, and shelter components:

Core goods prices have slipped into deflation as new and used auto prices have collapsed, with auto semiconductors more prevalent and logistics bottlenecks cleared. Services excluding shelter inflation have legged lower as COVID revenge travel and dine-outs moderate. Only rent inflation remains truly problematic, but of all the indicators, this lags the most. In fact, if we look at more concurrent indicators like the New Tenant Rent Index and the All Tenant Repeat Rent Index, we find rapid disinflation in rents that will ultimately register in CPI:

In sum, with goods inflation deflating, services ex-rents inflation dis-inflating, and rent poised to fall based upon more current indicators, inflation has clearly committed to a downward trend. Inflation gains over the last three months, annualized at closer to 3%, get us pretty close.

4th Quarter Earnings Yearnings

Earnings season began in earnest on Friday as the major money center banks released their fourth-quarter results. Analysts project S&P 500 earnings to fall 4%, the first quarterly decline since 2020. Only a small portion of the S&P 500 has reported results to date, but so far, the results have proven promising. Of the 29 companies that have reported, 79% have beaten estimates by 7.7%, on average. Should S&P 500 companies grow earnings in the fourth quarter rather than shrink them despite inflation declines, investors may see this as positive foreshadowing for 2023. If so, earnings resiliency spells investment opportunity, which will recalibrate expectations and rerating indices higher.

Have a great Sunday!

Sources: BLS, FRED Database, Bloomberg

">Inflation Deflates while Earnings Inflate… To Date!The Full Story:

Markets continued to punish the pessimists this week with the S&P 500 now over 4% higher in 2023. Last Friday’s wage disinflation report helped set the trajectory, while this week’s CPI report and better-than-expected earnings from the major banks helped maintain our course. Throughout the year, markets will fixate on the interplay between inflation and earnings. Remember, inflation actually boosts corporate earnings as higher prices drive higher revenues. When inflation falls, revenues fall, leading to corresponding compressions in earnings and, ultimately, stock prices. Analysts calling for disinflation and recession have marked down corporate earnings considerably. We are more optimistic, as corporate executives have had months to prepare for recessionary threats. Proposing that even in light of inflation and a potential recession, earnings resilience could surprise to the upside. This week provided two main data points to help resolve our dispute.

The Consumer Price Index Plunge

The U.S. Bureau of Labor Statistics released its December CPI report on Thursday morning. For the month of December, Consumer Price Inflation fell .1% versus November while gaining 6.5% over the past year. This stands well below the 9% reached in June but still well above the Fed’s 2% target. However, a deeper dig into the report reveals more weakness than the headlines might suggest. Consider the following 3-month average across the goods, services, and shelter components:

Core goods prices have slipped into deflation as new and used auto prices have collapsed, with auto semiconductors more prevalent and logistics bottlenecks cleared. Services excluding shelter inflation have legged lower as COVID revenge travel and dine-outs moderate. Only rent inflation remains truly problematic, but of all the indicators, this lags the most. In fact, if we look at more concurrent indicators like the New Tenant Rent Index and the All Tenant Repeat Rent Index, we find rapid disinflation in rents that will ultimately register in CPI:

In sum, with goods inflation deflating, services ex-rents inflation dis-inflating, and rent poised to fall based upon more current indicators, inflation has clearly committed to a downward trend. Inflation gains over the last three months, annualized at closer to 3%, get us pretty close.

4th Quarter Earnings Yearnings

Earnings season began in earnest on Friday as the major money center banks released their fourth-quarter results. Analysts project S&P 500 earnings to fall 4%, the first quarterly decline since 2020. Only a small portion of the S&P 500 has reported results to date, but so far, the results have proven promising. Of the 29 companies that have reported, 79% have beaten estimates by 7.7%, on average. Should S&P 500 companies grow earnings in the fourth quarter rather than shrink them despite inflation declines, investors may see this as positive foreshadowing for 2023. If so, earnings resiliency spells investment opportunity, which will recalibrate expectations and rerating indices higher.

Have a great Sunday!

Sources: BLS, FRED Database, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">High Five 2022

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Other asset classes that operate with a lag, like venture capital, private equity, and private debt, sharply marked down their values as well. Even housing prices found their way lower towards year-end. In short, only investors long in commodities stimulated by war profited in 2022. But that was last year.

2023: The Fed vs. Employers

The Fed has a mandate from Congress to throttle the US economy to a pace that maintains price stability and maximum employment. With the US unemployment rate at historic lows, half of the Fed’s Congressional mandate has been met. But with inflation at 7% versus the Fed’s 2% target, half of the Fed’s Congressional mandate has not been completed. Therefore, the Fed has a constitutional obligation to lower price levels. Since stimulus over-throttling in response to COVID caused excessive demand per unit of supply, the Fed must diminish demand. Structurally, 70% of the US economy is consumer based. If you want to lower consumer demand, you must lower consumer wages. But while CPI inflation has fallen over the past six months by 2% from 9% to 7%, wage inflation at 5% hasn’t budged. Getting this number down below 3% is the Fed’s primary objective for 2023. As investors learned in 2022, what the Fed wants, the Fed gets. Unfortunately, a rapid wage decline likely requires a rapid increase in the unemployment rate, meaning the Fed’s mandate to lower inflation has become an employer mandate to fire workers. While it may appear that employers are not complying with the headline as the unemployment rate is pegged at historic lows (3.5%), leading employment data tells us a different story.

Job openings have declined:

Weekly work hours per employee have declined:

Temporary labor levels have declined:

And overtime levels have declined:

So, while the lagging unemployment rate indicator remains hot, the leading unemployment indicators are cold. Employers have smartly begun complying with the Fed’s unemployment mandate; from here, it’s merely a question of pace. The faster employers shed labor and the faster wages fall, the sooner the Fed completes its disinflationary campaign. Therefore, the MOST IMPORTANT ECONOMIC INDICATOR FOR 2023 is the AVERAGE HOURLY EARNINGS report issued monthly by the Bureau of Labor Statistics (BLS). This report will arrive 12 times this year, on the first Friday of every month. Given the massive policy implications of each release, 2023 will feel like a 12-game playoff season for investors, with each release bound to drive significant upside or downside market volatility.

The first release, and therefore, the first wage playoff game results, arrived Friday morning. And the winner was… Investors!

Wage Playoff Game 1

Average Hourly Earnings fell significantly in December from a previously reported 5.1% to 4.6%, well below the 5% anticipated by economists. Furthermore, the BLS downgraded November’s average hourly earnings gain from 5.1% to 4.8%. These numbers firmly establish a declining wage trend, as seen in the chart below:

Remember, the Fed wants this number below 3%, likely closer to 2.5%. We will get there faster if employers cut more high-wage jobs proportionally than low-wage jobs. Note the opposite dynamic in the chart above. When COVID quarantine mandates forced consumer services businesses closures (retail, restaurants, theatres, etc.), lower wage unemployment levels skyrocketed. With the rapid elimination of lower-wage workers, average hourly earnings spiked 5%, even as the unemployment rate spiked 10%! It’s possible the opposite could occur now.

Given the structural scarcity of service laborers, employers might prefer eliminating bureaucratic redundancies, technology overstaffing levels, and tenured underperformers proportionately more. If so, the surprise for 2023 could be that wages fall faster than expected, the Fed pivots faster than expected, unemployment rises less than expected, and markets rise instead of fall, contrary to the consensus. It’s possible. But it’s also a long playoff season, and we have 11 more games to go.

Series score to date: Bulls 1, Bears 0.

Have a great Sunday!

Sources: BLS, FRED Database, Bloomberg

">Happy New Year?

Other asset classes that operate with a lag, like venture capital, private equity, and private debt, sharply marked down their values as well. Even housing prices found their way lower towards year-end. In short, only investors long in commodities stimulated by war profited in 2022. But that was last year.

2023: The Fed vs. Employers

The Fed has a mandate from Congress to throttle the US economy to a pace that maintains price stability and maximum employment. With the US unemployment rate at historic lows, half of the Fed’s Congressional mandate has been met. But with inflation at 7% versus the Fed’s 2% target, half of the Fed’s Congressional mandate has not been completed. Therefore, the Fed has a constitutional obligation to lower price levels. Since stimulus over-throttling in response to COVID caused excessive demand per unit of supply, the Fed must diminish demand. Structurally, 70% of the US economy is consumer based. If you want to lower consumer demand, you must lower consumer wages. But while CPI inflation has fallen over the past six months by 2% from 9% to 7%, wage inflation at 5% hasn’t budged. Getting this number down below 3% is the Fed’s primary objective for 2023. As investors learned in 2022, what the Fed wants, the Fed gets. Unfortunately, a rapid wage decline likely requires a rapid increase in the unemployment rate, meaning the Fed’s mandate to lower inflation has become an employer mandate to fire workers. While it may appear that employers are not complying with the headline as the unemployment rate is pegged at historic lows (3.5%), leading employment data tells us a different story.

Job openings have declined:

Weekly work hours per employee have declined:

Temporary labor levels have declined:

And overtime levels have declined:

So, while the lagging unemployment rate indicator remains hot, the leading unemployment indicators are cold. Employers have smartly begun complying with the Fed’s unemployment mandate; from here, it’s merely a question of pace. The faster employers shed labor and the faster wages fall, the sooner the Fed completes its disinflationary campaign. Therefore, the MOST IMPORTANT ECONOMIC INDICATOR FOR 2023 is the AVERAGE HOURLY EARNINGS report issued monthly by the Bureau of Labor Statistics (BLS). This report will arrive 12 times this year, on the first Friday of every month. Given the massive policy implications of each release, 2023 will feel like a 12-game playoff season for investors, with each release bound to drive significant upside or downside market volatility.

The first release, and therefore, the first wage playoff game results, arrived Friday morning. And the winner was… Investors!

Wage Playoff Game 1

Average Hourly Earnings fell significantly in December from a previously reported 5.1% to 4.6%, well below the 5% anticipated by economists. Furthermore, the BLS downgraded November’s average hourly earnings gain from 5.1% to 4.8%. These numbers firmly establish a declining wage trend, as seen in the chart below:

Remember, the Fed wants this number below 3%, likely closer to 2.5%. We will get there faster if employers cut more high-wage jobs proportionally than low-wage jobs. Note the opposite dynamic in the chart above. When COVID quarantine mandates forced consumer services businesses closures (retail, restaurants, theatres, etc.), lower wage unemployment levels skyrocketed. With the rapid elimination of lower-wage workers, average hourly earnings spiked 5%, even as the unemployment rate spiked 10%! It’s possible the opposite could occur now.

Given the structural scarcity of service laborers, employers might prefer eliminating bureaucratic redundancies, technology overstaffing levels, and tenured underperformers proportionately more. If so, the surprise for 2023 could be that wages fall faster than expected, the Fed pivots faster than expected, unemployment rises less than expected, and markets rise instead of fall, contrary to the consensus. It’s possible. But it’s also a long playoff season, and we have 11 more games to go.

Series score to date: Bulls 1, Bears 0.

Have a great Sunday!

Sources: BLS, FRED Database, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">The New Powell Pivot

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">The Drive For 5

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">Powell Claus

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">Rally Reasons for the Season

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">The FOMO Rally!

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

" class="link-chevron">

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist

Sources: JPMorgan, Edward Jones, Bloomberg

">A Letter from the Tax Conference

Friday’s report should reinforce expectations that the Fed will accelerate the tapering of Quantitative Easing at its meeting this next week and potentially raise rates as soon as June 2022. Naturally, some investors fear equity market volatility as the Fed starts to reduce liquidity injections into the system and embarks on a rate-hiking cycle; however, equities historically have held up well during tapering and the start of Fed rate hikes. It is only toward the end of Fed cycles that we tend to get more serious volatility, which is unlikely to be in the next 18 months.

I also think it’s noteworthy that Jerome Powell started his term as Fed Chair in February 2018 and presided over the last cycle of rate hikes including the overtightening and resulting stock market correction during the fourth quarter of 2018. I’m hopeful that lessons were learned.

Omicron

The Omicron variant of Covid-19 first became a news headline and market concern on the day after Thanksgiving and the following week. The S&P 500 saw its worst 2-day performance in over a year and the Volatility Index rose to above 30 for the first time since February. Also, that same week in testimony before Congress, Fed Chair Jerome Powell suggested that inflation was no longer transitory and that the pace of tapering might be accelerated at the Fed’s December meeting. Both contributed to market stress and the risk-off selling mentioned previously.

Thankfully, Omicron-induced pressure has been slightly easing. On Friday, the CDC released a report on the first studied cases in the U.S. and many of the omicron variant infections appear to be mild. They did note that it was a very small sample size (43 cases), it can take several days or weeks before severe symptoms appear in some individuals, and symptoms would be expected to be milder in infected vaccinated people and in those with a previous coronavirus infection.

The CDC report aligns with similar early reports from South Africa. The South African Medical Research Council reported that most hospitalized patients who tested positive did not need supplemental oxygen, few developed pneumonia, few required high-level care, and few were admitted to intensive care. The average length of hospital stays was below 3 days, compared to 8.5 days over the last 18 months.

BioNTech and Pfizer expect to deliver an Omicron-specific vaccine by March 2022. The companies also reported that in laboratory tests, a three-shot regimen (including the booster) may be just as effective in neutralizing the new Omicron variant as their original two-shot regimen was in neutralizing Alpha.

While it seems highly unlikely that we were ever headed back into a lockdown, social distancing restrictions impacting hospitality, leisure, food & beverage, and entertainment industries as well as the availability of workers all have real economic impacts.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist